Global aviation continues to reflect the structure of the world economy: scale, domestic market depth, and route density remain the primary drivers of passenger dominance.

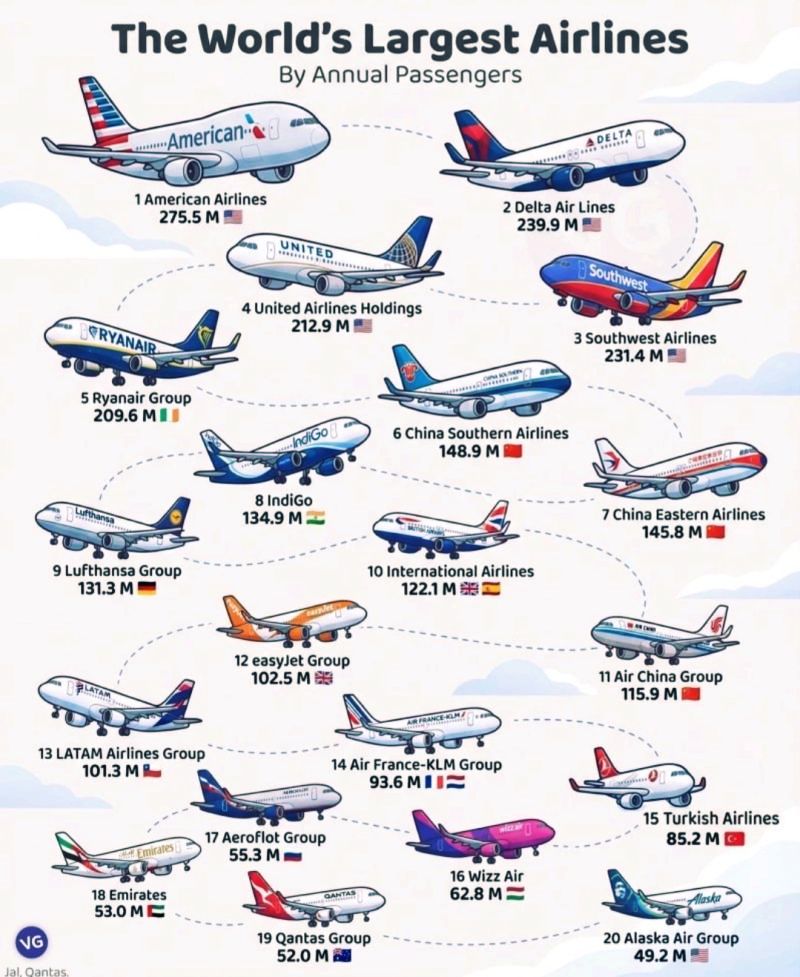

The latest rankings highlight a clear concentration among U.S. carriers. American Airlines, Delta Air Lines, and Southwest Airlines collectively transport hundreds of millions of passengers annually, benefiting from the size of the U.S. domestic market, strong hub-and-spoke systems, and consistent demand across business and leisure segments.

Europe maintains a strong presence through low-cost champions and legacy groups. Ryanair and easyJet demonstrate how efficiency, frequency, and competitive pricing can drive volume leadership across a fragmented continent, while Lufthansa Group and Air France-KLM continue to anchor intercontinental connectivity.

Asia is increasingly influential. China Southern, China Eastern, and Air China illustrate the sheer scale of regional mobility, supported by urbanization, rising middle-class travel, and expanding airport infrastructure. IndiGo’s rapid growth further confirms India’s emergence as one of the fastest-expanding aviation markets.

Meanwhile, global connectors such as Emirates, Turkish Airlines, and Qantas focus more on long-haul strategy and premium transit positioning rather than pure passenger volume, yet remain essential nodes in intercontinental mobility.

From an investment and macro perspective, aviation passenger rankings offer insight into:

* The strength of domestic consumption

* Tourism flows and business travel recovery

* Infrastructure development priorities

* Competitive positioning of airline business models

Airlines are not just transport companies — they are real-time indicators of economic dynamism, mobility trends, and globalization intensity.

Source: TicketVisa.com